By Marco Polo Viana

By Marco Polo Viana

Registering product information is an important step in any business, as it directly influences inventory quality and the efficiency of commercial operations.

The tax reform brings significant changes to taxation and classification of operations and goods in company operations.

In this article, we will explain some guidelines and impacts of the new classification of operations and goods.

What is merchandise classification?

Classifying goods technically and fiscally means identifying, in the Catalogue of the Harmonized System of Designation and Coding of Goods (six digits) and in the Common Nomenclature of MERCOSUR (eight digits), the code that best represents the product under analysis.

This identification allows for the correct classification of goods in import, export, and commercialization operations, ensuring compliance with tax procedures. Furthermore, correct classification is essential for determining the applicable tax burden and ensuring the proper application of legal regulations.

The Harmonized System and the NCM

Given the existence of hundreds of thousands of different goods in the world and the peculiarities and languages of each country, the World Customs Organization (World Custo Organization – WCOThe Harmonized System, which today has 183 members (as of 2018), conceived the Harmonized System, enabling the standardization of a worldwide code for each commodity that can be traded.

Based on this extensive catalog of goods, the Harmonized System, where each good is identified by a code, each member country creates its own table, maintaining the original structure of the Harmonized System.

Example: In Brazil and MERCOSUR, item 3926.90.10 was created to identify plastic washers. Brazil also adopts, in addition to these eight digits, the expression Ex (Exclusively), aiming to subdivide the eight-digit code, whether due to the need to differentiate tax rates, incentives, benefits, or for another reason.

Code 3926.90.40 refers to "Laboratory or pharmacy articles," however, if these articles are intended "Exclusively" for clinical analysis laboratories, the code will be 3926.90.40 Ex 01.

Tax Classification

Correct tax classification depends on clearly understanding what the merchandise is, what it's used for, what it's made of, and whether it has its own function or complements another. Often, it's a part or component of another product and may receive the same code or a specific code, depending on the case.

Therefore, it is important to analyze the general rules, explanatory notes, and position descriptions to ensure accurate classification and avoid tax errors.

Each product has its own particularities, as is the case with food, which varies according to preparation, state (raw, fried, frozen) and type of packaging. Parts also differ: some have multiple uses, such as screws, while others serve a single application.

The higher the level of industrialization, the higher the chapter number and tax code — for example, live animals (01.06) are at the beginning of the chain, while nuclear reactors (84.01) represent more complex products. After studying these characteristics, the Tax Classification begins, identifying the correct position and sub-position in the Harmonized System and the complete code in the NCM/TEC/TIPI.

Tax Classification of Transactions in the Tax Reform

With the implementation of the IBS (Tax on Goods and Services) and the CBS (Contribution on Goods and Services) From January 2026 onwards, one of the biggest challenges for companies and tax professionals will be the correct tax classification of transactions and products.

The new code cClass Trib (Tax Classification Code) It replaces the old CST/CFOP logic and requires a more in-depth analysis of each transaction, considering its... onerousness, consideration and the tax incidence matrix rule defined by Complementary Law No. 214.

Contrary to what many imagine, it is not possible to create a simple “from/to”"between NCM and cClassTrib. The classification depends on a contextual reading of the operation, the nature of the revenue, and the possible application of exceptions or reductions provided for in the legislation.".

To assist in this process, the use of automated solutions that cross-reference legal rules and product descriptions, optimizing the mapping and definition of cClassTrib at scale, can be of great help.

Identification of cClassTrib for Operations with IBS and CBS

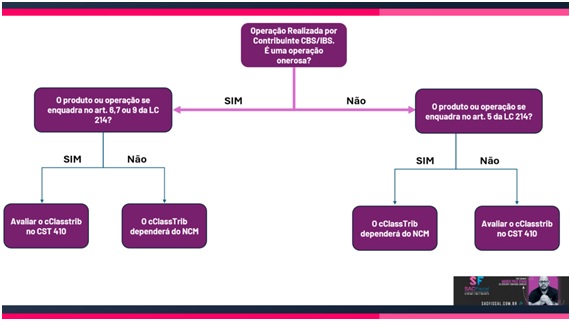

O cClassTrib This is the new code that identifies the tax treatment of each transaction and product within the scope of the IBS and CBS. Its definition It's not automatic. — requires an understanding of Complementary Law 214, which establishes the incidence structure and the exceptions. The classification process goes through three main stages:

- Identifying the onerous nature of the operation (whether it is onerous or not).

- Verification of occurrence or non-occurrence based on general rules and legal exceptions.

- Consultation of the NCM and annexes of Complementary Law 214, to check for specific tax rate reductions or exemptions.

Each cClassTrib is a "child" of a CST — for example, the CST 410 brings together operations not onerous in non-incidence or immunity, while the CST 000 groups fully taxed transactions.

The starting point for any classification is to identify whether the operation is... expensive (with consideration) or not onerous (without consideration).

- Costly OperationsAs a rule, suffer from IBS and CBS incidence., except for the exceptions provided for in articles 6, 7 and 8 of LC 214.

- Non-Onerous OperationsAs a rule, They do not suffer from the incidence., But there are exceptions — such as bonuses, gifts and free supplies which may be taxed in accordance with Article 5.

This distinction is essential because it defines the classification path — the CST and, consequently, the cClassTrib.

Application of the Rules of Incidence and Exceptions of LC214/2025

THE Complementary Law No. 214/2025 establishes rules of incidence of the new taxes on consumption and also the exceptional circumstances. Examples of exceptions include:

- Exports of goods and services (immune – art. 8º);

- Supplies provided free of charge, like gifts and bonuses, which may or may not be taxed depending on whether or not they appear on the tax document (art. 5º);

- Supplies at a value lower than the market price, when characterized as a non-onerous taxable transaction (art. 5, I).

Therefore, each transaction needs to be analyzed in light of the regulations—the CFOP or NCM code alone is not enough: the context and purpose determine the tax treatment.

After identifying the nature of the operation, the next step is to verify the NCM (Common Nomenclature of Mercosur) of the product and consult the annexes of LC 214.

These annexes provide specific tax rate reductions, such as:

- Annex 1 – Basic food basket products (reduced to zero);

- Annex 5 Accessibility devices for people with disabilities;

- Other attachments Medicines, books, education, public transport, etc.

Non-onerous operations:

Those are the ones without financial compensation, such as donations, free transfers and remittances with no commercial value.

- In general: There is no incidence of IBS and CBS.

- Exceptions: must be evaluated according to the Article 5 of LC 214

- When non-incidence is confirmed → it may apply to the cClassTrib of CST 410

costly operations:

They involve economic consideration, That is, exchange, sale or provision of services in exchange for payment.

- In general: there will be incidence of IBS and CBS

- Exceptions: as provided in Articles 6, 8 and 9 of LC 214

- The CST varies according to NCM of the product or service, Because taxation depends on the tax classification.

In this classification simulation, our evaluation premises are the CFOP code for the transaction (although there is no CFOP code in IBS and CBS, it indicates what the transaction is about), the NCM code of the merchandise, whether it is a transaction for a public entity, and whether it is a transaction for the Manaus Free Trade Zone/Alcohol Free Trade Zone.

Based on these premises, we arrive at the CST, cClasstrib, type of taxation, tax rates, and legal basis.

This article summarizes the legal-tax reasoning which the professional must apply in their classification of operations and merchandise under IBS and CBS. This reasoning is fundamental for the parameterization of tax rules in the ERP, especially in modules of automated tax classification, such as tax compliance solutions.

Marco Polo Viana is the Director of SACFiscal & Automation

Notice: The opinion presented in this article is the responsibility of its author and not of ABES - Brazilian Association of Software Companies